Is Whole Life Insurance a Smart Investment or Just a Basic Safety Net?

When considering whole life insurance, many individuals grapple with its dual purpose: as a safety net and an investment vehicle. On one hand, whole life insurance provides a guaranteed death benefit, offering peace of mind for policyholders and their beneficiaries. This aspect positions it as more than just an insurance product; it's a significant layer of financial security. However, critics argue that the investment component of whole life policies, which includes cash value accumulation, may not yield returns comparable to other investment options such as stocks or mutual funds. In fact, research from NerdWallet suggests that the cost of premiums may outweigh the benefits for many individuals.

Ultimately, deciding whether whole life insurance is a smart investment depends on your financial goals and circumstances. If you seek lifelong coverage with a guaranteed payout, it could serve well as a basic safety net. However, if your primary aim is to grow your wealth, alternatives like term life insurance coupled with separate investments might better align with your objectives. Before making a decision, consulting resources like Investopedia can provide deeper insights into the pros and cons, helping you evaluate whether this financial product meets your needs.

Understanding the Benefits and Drawbacks of Whole Life Insurance

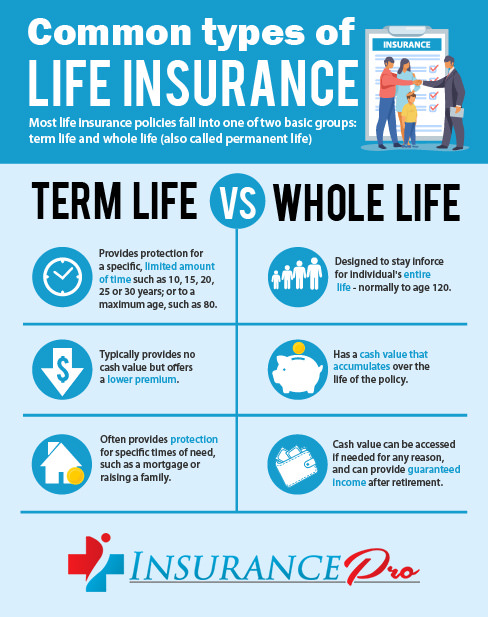

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as premiums are paid. One significant benefit of whole life insurance is that it builds cash value over time. This cash value grows at a guaranteed rate, allowing policyholders to borrow against it or withdraw funds, offering a safety net during financial emergencies. Additionally, whole life policies often come with predictable premiums and guaranteed death benefits, ensuring that beneficiaries receive a financial payout upon the policyholder's death.

However, there are also notable drawbacks to consider. Whole life insurance policies typically have higher premiums compared to term life insurance, which can strain budgets, particularly for young families or those just starting out financially. Furthermore, while the cash value component is appealing, it can take several years for the cash value to accumulate significantly, as highlighted by experts at Forbes. Consequently, individuals should evaluate their financial situation, needs, and long-term goals before committing to a whole life policy.

How Whole Life Insurance Fits into Your Financial Planning Strategy

Whole life insurance is often viewed as a crucial component of a well-rounded financial planning strategy. Unlike term life insurance, which provides coverage for a specific period, whole life insurance offers lifelong protection and grows cash value over time. This dual benefit makes it an appealing choice for individuals seeking to build wealth while ensuring that their loved ones are financially secure in the event of an untimely death. By incorporating whole life insurance into your financial plan, you can create a diversified portfolio that includes both risk management and savings elements. For more insights, you can visit Investopedia.

Furthermore, the cash value component of whole life insurance can serve as a valuable financial resource. Policyholders can borrow against the cash value, providing a source of funds for major life expenses such as education, a new home, or retirement. This feature offers flexibility and can enhance your overall financial strategy. However, it's essential to understand the terms associated with borrowing against your policy, as it can impact the death benefit. To learn more about managing your policy effectively, check out NerdWallet.