Understanding Whole Life Insurance: Is It Worth the Investment?

Whole life insurance is a type of permanent life insurance that provides lifetime coverage and has a cash value component. Unlike term life insurance, which only covers you for a specific period, whole life insurance guarantees a death benefit to your beneficiaries as long as the premiums are paid. This policy accumulates cash value over time, which can be borrowed against or withdrawn, making it a unique investment opportunity. For many individuals, understanding the mechanics of whole life insurance can help in determining if it is a worthwhile addition to their financial portfolio.

When considering the value of whole life insurance, it's essential to evaluate both its benefits and drawbacks. On the one hand, whole life insurance offers stability, predictable premiums, and a guaranteed cash value growth that can serve as a safety net for emergencies or supplemental retirement income. However, it's crucial to note that the premiums are typically higher than those of term life policies, which can strain budgets. Ultimately, the decision to invest in whole life insurance should be based on an individual's financial goals, risk tolerance, and the need for long-term financial security.

Whole Life Insurance vs. Term Life: Which is Right for You?

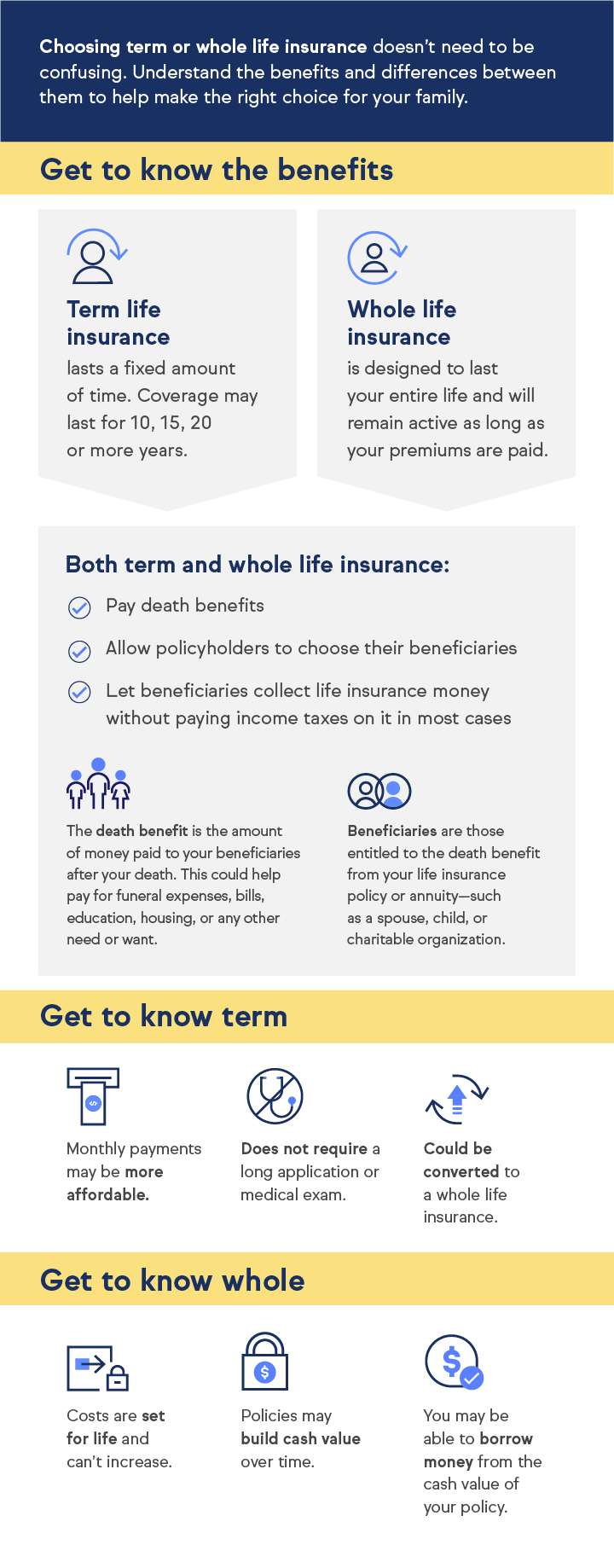

Whole life insurance and term life insurance are two popular types of life insurance that serve different financial needs. Whole life insurance provides coverage for your entire lifetime, as long as you continue to pay the premiums. It also accumulates cash value over time, which you can borrow against or withdraw. On the other hand, term life insurance offers coverage for a specified period, usually between 10 to 30 years, and is often more affordable. This makes it a suitable choice for those who need coverage during critical financial years, such as raising children or paying off a mortgage.

When deciding between the two, consider your financial goals and circumstances. If you are looking for a policy that builds cash value and lasts a lifetime, whole life insurance may be the right fit. However, if you require a cost-effective solution to provide financial protection for a limited time, term life insurance might be the better option. Ultimately, your decision should reflect your financial situation, long-term goals, and comfort level with premiums. Analyzing your needs and consulting with a financial advisor can help ensure you choose a policy that aligns with your objectives.

The Benefits and Drawbacks of Whole Life Insurance: What You Need to Know

Whole life insurance provides several benefits that make it an attractive option for individuals seeking long-term financial security. One of the primary advantages is the guaranteed death benefit, which ensures your beneficiaries receive a predetermined amount upon your passing. Additionally, whole life policies accumulate cash value over time, which can be accessed through loans or withdrawals, thus providing a financial safety net in times of need. This accumulation of cash value is tax-deferred, meaning policyholders won't owe taxes on the gains as they grow, allowing for exponential growth over the years.

However, there are also notable drawbacks to consider with whole life insurance. One major concern is the cost; <whole life premiums can be significantly higher than term life insurance, which may not fit every budget. Moreover, the returns on the cash value component often lag behind alternative investment options, leading some consumers to question the wisdom of tying up funds in a policy. It's essential for potential policyholders to weigh these benefits and drawbacks thoroughly, ensuring that they align with their financial goals and risk tolerance.